M&A activity continued to slump during the second quarter. Technology companies, which are often a primary driver of activity, continue to stagnate, with Goldman Sachs analyst Sam Britton predicting as much as an 80% drop in tech M&A this year, “as an economic slowdown and a hostile anti-trust environment weighed on dealmaking appetite.” The banking crisis has eased and regulatory enforcement actions are actually down, but higher interest rates and geopolitical turmoil continue to weigh on companies’ risk tolerances. Matterhorn’s M&A database tracks publicly-announced US deals over $25 million in value, harnessing both AI and attorneys to digest the granular deal points of each transaction to allow for comparisons across industries, specific deal terms, and both legal and financial advisors.

While far from the M&A boom of 2021, many notable deals were announced – particularly ONEOK, Inc.’s blockbuster acquisition of Magellan Midstream Partners, L.P. The $60 billion deal combined the energy infrastructure giants in May. The deal propelled the top two firms far ahead of the rest of the pack.

Latham & Watkins jumped from the #5 spot last quarter to handily lead the field with 5 large deal announced in addition to ONEOK/Magellan Midstream Partners. Other notable deals include Merck & Co., Inc.’s acquisition of Prometheus Biosciences, Inc. and Elliott Investment Management’s acquisition of Syneos Health, Inc.

Kirkland dropped from the #1 stop last quarter but still advised on a whooping 8 deals valued at nearly $72 billion. Paul Weiss, which sat across from Latham on the Merk/Prometheus deal, comes in at a distant third place with 7 deals announced valued at nearly $32 billion.

Frequent list-leader Wachtell dropped one spot this quarter to 4th place, with 8 deals announced valued at nearly $29 billion. Finally, Skadden rejoined the league table this quarter at 5th place with 6 deals announced valued at over $22 billion.

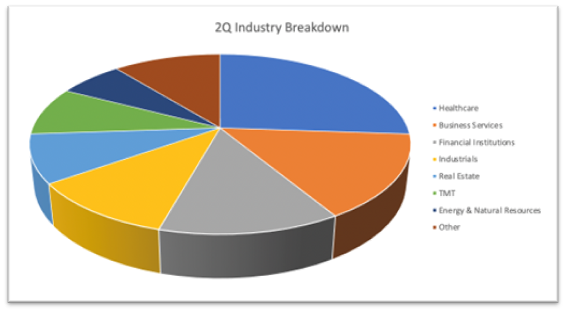

Analyzing the industry breakdown of deals this quarter, it is especially noteworthy that the technology, media, and telecom (TMT) segment has dropped to a mere 8.7% share of deals announced, landing at 6th place, down from 3rd just last quarter. Healthcare continues to lead the pack with 26% of deal announced from that industry. While industrials have scaled back this quarter, business services deals have rushed in to take their place.

The future may be brighter. For the remainder of 2023, “sturdy shoots of optimism can be found,” according to McKinsey. “Some deal makers question why the global M&A market would depart from a pattern established over eight years, which shows mostly stable deal value on an annual basis.” At the European M&A conference co-hosted by McKinsey and Goldman Sachs, over 50% of participants surveyed in February stated that they plan to increase their M&A activity or other transformative deals in 2023. It remains to be seen whether their expectations will become reality.