Everbridge, Inc., a leader in national public warning solutions, announced it will be taken private via an acquisition by software investment firm Thoma Bravo. The $1.5 billion all cash deal will remove Everbridge from the Nasdaq and is expected to close during the first half of 2024.

“Everbridge was founded in the aftermath of 9/11 with the mission of helping to keep people safe and organizations running amid critical situations,” according to the company’s press release. “Its suite of Software-as-a-Service (SaaS) products encompassing mass notification, IT incident management, travel risk management, physical security information management, population alerting, and risk intelligence, has positioned Everbridge as a trusted partner to meet the evolving needs of a diverse base of 6,500+ customers.”

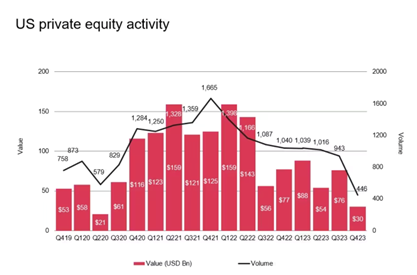

The deal arrives as private equity activity has slumped for the past year and a half. After peaking in 2021 through early 2022, private equity activity dropped off precipitously in the second half of 2022 and remained low throughout 2023. The high interest rates and capital costs that have accompanied persistently high inflation and geopolitical turmoil since 2022 has made investors cautious. Private equity firms have largely responded by waiting on the sidelines waiting for lower valuations as the economy cools.

While they await more attractive deals, such as this one, private equity firms have amassed an unprecedented an unprecedented $2.59 trillion in cash reserves (i.e. “dry powder”). “Record dry powder accumulation is rooted in the robust M&A market of the last several years, which set high valuation expectations for sellers that remained elevated even as macroeconomic conditions increasingly slowed deal activity from 2022 onward,” as Chris Zochowski, a private equity partner at Shearman & Sterling explained to S&P Global. “Buyers want lower asset prices, and the resulting valuation gap creates hesitancy to execute deals.”

There is still opportunity for other private equity shops to deploy some of that dry powder to acquire Everbridge. According to DealPulse’s M&A database, which harnesses both AI and attorneys to digest the granular deal points of each publicly-announced transaction over $25 million, the company’s agreement and plan of merger with Thoma Bravo permits a 25-day go-shop period where Everbridge is permitted to solicit other offers. This is a relatively short go shop period: over the past 22 months, the averge go shop period was over 30 days.

Everbridge is advised by law firm Cooley LLP, and financial adviser Qatalyst Partners. Thoma Bravo is advised by Kirkland & Ellis LLP.