As the U.S. banking sector continues to consolidate, community banks First National Corporation and Touchstone Bankshares, Inc. announced plans to merge. First National will acquire Touchstone in an all-stock deal valued at $47 million that is expected to close in Q4 2024.

“The combined company will bring together two community banks with a deep commitment to the customers and communities they have each served since the early 1900s,” according to the banks’ joint press release. “Total assets are expected to be approximately $2.1 billion, with $1.5 billion in loans, $1.8 billion in deposits, thirty branch offices across Virginia and two branches in North Carolina. The resulting company is expected to be the ninth largest Virginia community bank as ranked by deposits.”

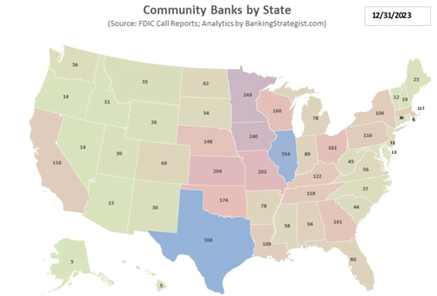

The U.S. banking system is quite diffuse compared to other developed countries. Of the over four thousand FDIC-insured institutions, the vast majority are community banks. Although the top 10 banks wield 53% of assets, these behemoths account for a mere 24% of bank branches across the country.

While there is no precise definition of what constitutes a community bank vs. a regional or large bank, the FDIC generally characterizes community banks as those with less than $10 billion in assets. These smaller banks typically obtain most of their core deposits locally and likewise make their loans to local businesses and consumers. These banks are often provide better and more personalized customer service: a 2019 Small Business Credit Survey found that of the small business owners who applied for loans with community banks, 79% were satisfied with the experience, compared with 67% of those who applied at large banks.

Regional banks are generally defined as banks holding $10- $100 billion in assets, while large banks are those with over $100 billion. There were 4,001 community banks across the U.S., boasting over 27,511 branches, as of December 2022. This is compared to just 134 regional banks with 13,109 branches, and 31 large banks with 30,570 branches.

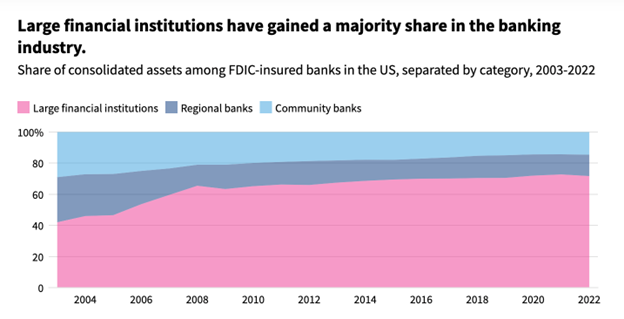

The number of community banks has steadily dwindled, however. “While the number of U.S. banks has consistently contracted every year since at least 1984 by an average of 3.3% per year, the trend has accelerated post-Great Financial Crisis, with a 4.0% average annual reduction in the number of commercial banks in the period since 2011,” according to Fitch. “Under an assumption of 3% annual attrition between 2020 and 2030, we are likely to see an approximate reduction in the number of banks during that period of 26%.”

This consolidation is driven largely by competition for deposits along with increasing technology expenses. As smaller banks seek to keep up larger banks’ technologies, including loan application and underwriting software along with mobile banking, the associated costs drive banks towards economies of scale. First National/Touchstone Bankshares merger is the latest example.

According to DealPulse’s M&A database, which harnesses both AI and attorneys to digest the granular deal points of publicly announced transactions, Touchstone Bankshares is advised by Williams Mullen and First National is advised by Nelson Mullins Riley & Scarborough LLP.