Also called a “blank check” company, a Special Purpose Acquisition Company (SPAC) is a shell corporation created to acquire a private company and take it public while sidestepping the rigors and delays of a traditional initial public offering (IPO). Though they have no operations of their own, SPACs are listed publicly on a stock exchange and have no specific business purpose other than to pool funds and acquire another company.

Most often, a SPAC is formed by sponsors who have expertise in a certain industry and seek out companies in that area – but even if they have a target company in mind, they do not identify it so that they do not need to disclose those details during the SPACs IPO process. This is where the “blank check” comes from: the SPAC provides its IPO investors little information. Despite this lack of detail, SPACs often sign up large, prominent institutional investors and underwriters prior to offering their shares publicly. These investors trust the ability of the SPAC’s promoters to secure a good target for their investment.

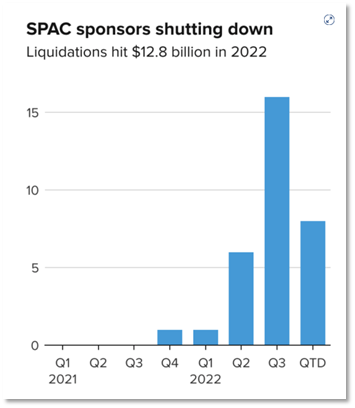

While the SPAC pursues its target, these investors’ funds sit in an interest-bearing trust. The investment vehicles have an expiration date, however; if the SPAC has not completed a deal within a certain time period (typically two years), it faces liquidation and the outstanding cash is returned to the investors. Such liquidation has become increasingly common since the summer of 2022 when economic and market conditions made finding advantageous deals increasingly difficult. Further, SPAC’s that return fund to their investors can face a 1% excise tax starting in 2023, prompting some sponsors to liquidate before year end.

If the SPAC successfully finds a target company, the sponsors negotiate with that company, and then if the SPAC’s shareholders approve of the deal, the SPAC merges with the target. This enables the target company to go public while avoiding the time and regulations of the traditional IPO process. While it typically takes companies 6 months to a year to adhere to the processes and disclosures required of an IPO, the target company can go public in mere months via closing a merger with a SPAC. Most often, the SPAC acquires the target in a reverse merger,with the target merges into the SPAC or its subsidiary. Then, the combined company typically renamed with the target’s name and the SPAC’s ticker changed. The target’s business operations then live on as a publicly traded company with additional funds from the investment.

SPACs boomed in 2020 and throughout 2021, with well-known names from Channing Tatum to President Donald Trump making headlines due to their involvement with these investment vehicles. The SEC responded by issuing an investment alert stating, “It is never a good idea to invest in a SPAC just because someone famous sponsors or invests in it or says it is a good investment.”

History

SPACs are far from a new financial innovation: they date back to the 1993 when David Nussbaum and lawyer David Miller created the first SPAC to enable private companies to access a broader pool of investors.

While the investment vehicles remained relatively obscure for decades, they finally boomed during the pandemic as a confluence of factors propelled the current surge: the Federal Reserve’s interest rate cuts during the start of the covid 19 shutdowns flooded markets with cash, incentivizing investors to pour funds into SPACs in search of returns. And just as cash was flowing into public markets, the number of public companies had dropped significantly over the preceding decades, declining from 8000 to 4000.

In turn, SPACs used the hedge fund and other investors’ funds by identifying private companies ripe for public markets. The early successes of Virgin Galactic and DraftKings fueled SPACs’ popularity. Private equity funds have also jumped in on the action increasingly during the past few years, with PIPE (private investment in public equity transactions) deals, such as SoundHound, Inc., further fueling SPAC deals.

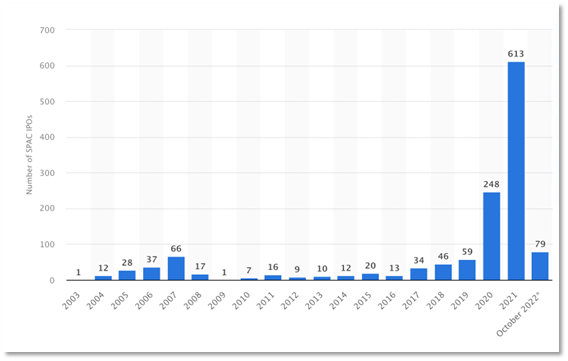

SPAC IPOs in the United States, 2003 – October 2022

Scrutiny

SPACs came under attack starting in 2021 from both shareholders and regulators. Shareholders filed multiple high profile class action lawsuits alleging the investment vehicles made false claims and did not properly disclosure information.

Meanwhile, the SEC launched multiple investigations (see e.g. SEC Charges Perceptive Advisors for Failing to Disclose SPAC-Related Conflicts of Interest) into certain SPACs as SEC Chairman Gary Gensler has made clear his goal of cracking down on SPACs and introducing further regulations. Law firms jumped to SPACs’ defense, arguing that they are merely operating companies rather than investment vehicles and should therefore not be regulated as the latter.

Future

Although they may have lost their luster in recent months, SPACs will be around for the foreseeable future. Over just the past month, multiple companies have gone public via SPAC acquisition (see e.g. FlexJet and flyExclusive). Analysts expect that with improved disclosures and diligence practices, SPACs will remain a popular alternative to traditional IPOs in the years to come.