M&A deal activity boomed during 2021, with global M&A and related deal activity surpassing $5 trillion for the first time in history. 98 deals closed in the United States in Q4, representing $238 billion in activity.

While this represents a 34% increase in the number of deals closed in the US compared to Q3, it is a 30% decline in valuation as fewer mega-deals were announced during the quarter. While strong by broader historical standards, this pace is a far cry from the blistering activity of 4Q 2020, as the economy reopened following the 2020 lockdowns. Matterhorn’s M&A database tracks publicly-announced deals over $25 million in value, harnessing both AI and attorneys to digest the granular deal points of each transaction to allow for comparisons across industries, specific deal terms, and both legal and financial advisors.

Latham & Watkins tops the league table this quarter, propelled by the largest deal of the quarter: Oracle’s $28.3 billion acquisition of Cerner Corporation announced December 30. Whether advising the acquirer or target company, Latham appeared in the deal documents for just 8 of the 98 deals closed, valued at $43.75 billion. 2021 was a banner year for Latham, which finished 3rd on the Q3 tables. Latham’s large deals enabled the firm to narrowly edge out Skadden, which advised on 13.2% of all deals announced, valued at $43.68 billion. Skadden had fallen off the Q3 tables but came roaring back this quarter by advising on 16 deals announced.

Propelled by Emerson Electric’s $11 billion acquisition of Aspen Technology, Davis Polk rounded out the top three. DPW had a hand in 9% of deals closed during the quarter, accounting for $29 billion. Sitting opposite Latham on the Oracle/Cerner deal, Hogan Lovells joined the league table this quarter with that single mega-deal.

Wachtell rounds out the top 5 firms in Q4, narrowly besting Fried Frank. Wachtell advised on 6 deals, representing $21.7 billion in value. While Kirkland & Ellis lead the league tables in Q3, it dropped off the table during Q4 as it did not advise on the same staggering number of deals that it had during Q3.

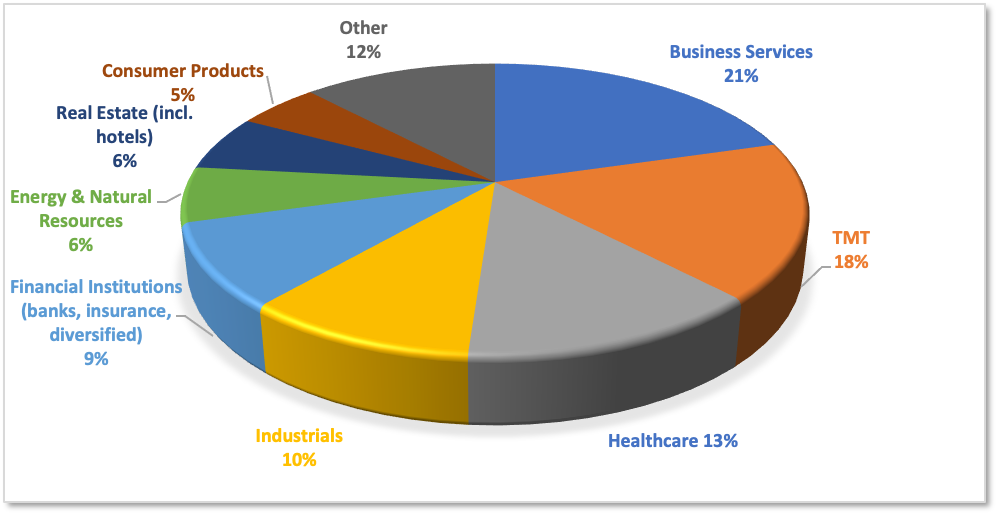

Certain industries were in higher demand than others this quarter as target companies in business services accounted for 21% of all activity, followed by TMT deals, which made up 18%. Along with healthcare, these top three industries accounted for a majority of all M&A transactions closed during the period.

Industries

While largely in line with deal activity in the final quarter of 2019, Q4 2021 fell well below the surge of Q4 2020, when 131 deals closed before the second wave of the pandemic struck. Analysts anticipated that the M&A boom will continue – and even accelerate – in 2022.