In the latest blockbuster energy deal, ConocoPhillips’s announced it will acquire independent oil and gas producer Marathon Oil for $22.5 billion. The all-stock deal is the latest in a wave of multibillion deals in the industry, including Crescent Energy Company’s $2.1 billion takeover SilverBow Resources, Inc. last month, as well as California Resources’ $2.1 billion acquisitions of Aera Energy LLC and APA Corporation’s $4.5 billion merger with Callon Petroleum Company earlier this year.

“This acquisition of Marathon Oil further deepens our portfolio and fits within our financial framework, adding high-quality, low cost of supply inventory adjacent to our leading U.S. unconventional position,” Ryan Lance, ConocoPhillips chairman and chief executive officer, stated in the deal’s press release.

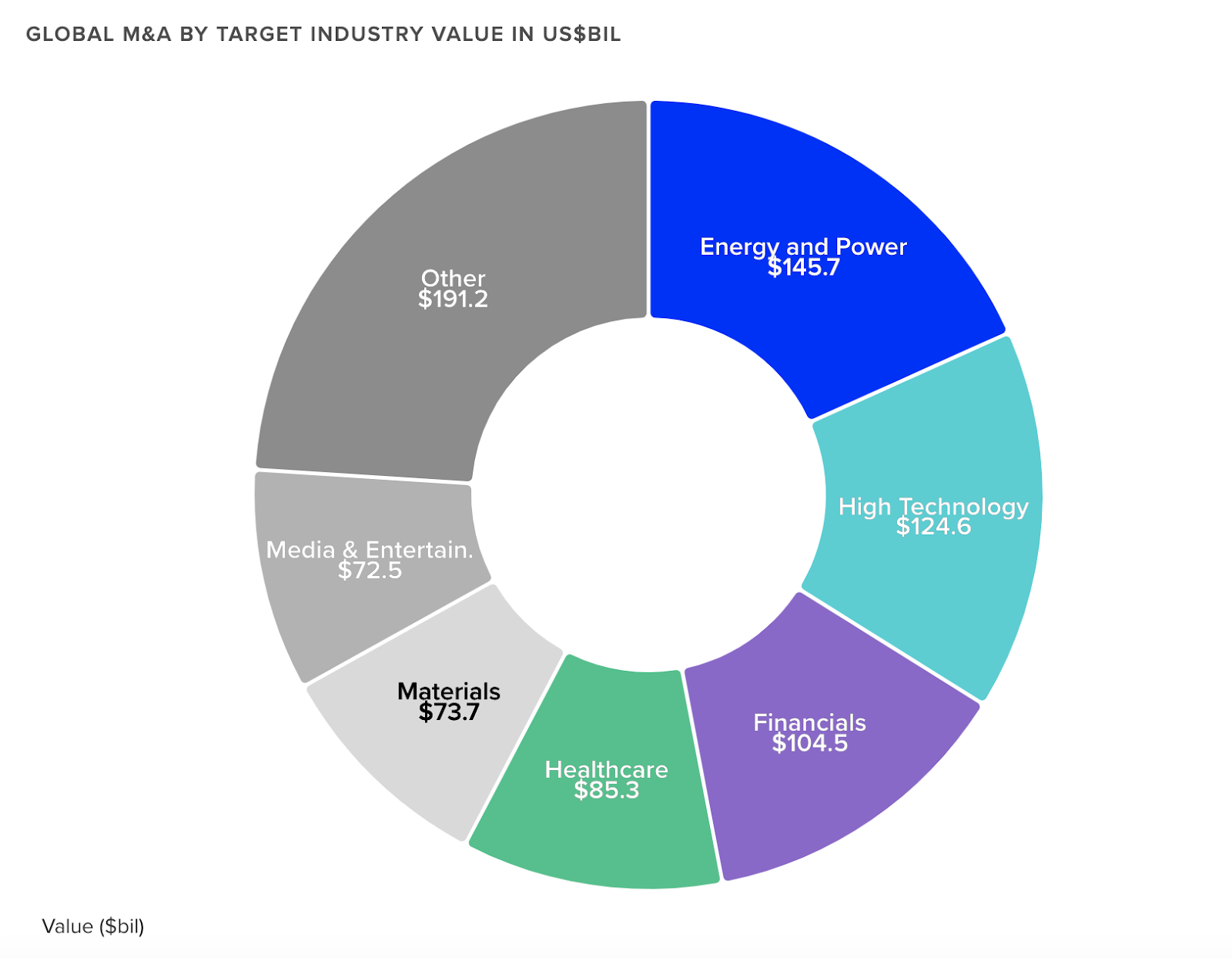

Source: LSEG

This deal is part of a pattern of consolidation in the industry as oil giants deploy their large cash reserves – as was the case with Exxon’s $64.5 billion acquisition of Pioneer Natural Resources. While the size of Exxon’s acquisition will likely draw the attention of regulators, ConocoPhillips is more likely to pass regulatory muster.

President Biden has vowed additional antitrust scrutiny, blaming rising prices on a lack of competition, and appointed enforcement-minded individuals to lead the Federal Trade Commission (FTC). Last December, the DOJ and FTC released the 2023 Merger Guidelines, which “lower the threshold market concentration level at which the agencies would presume a merger to be illegal,” according to Paul Weiss. “The new guidelines also include a new presumption that a merger resulting in the merged firm having a market share greater than 30% would be illegal if it also resulted in a relatively modest increase in market concentration.”

According to Ed Hirs, senior fellow at the University of Houston, this ConocoPhillips/Marathon deal is not likely to face antitrust action. He points out, “The two companies together are still smaller than the majors . . . . They are both independent oil companies without any downstream assets for refining, distribution, and retail.” While Exxon’s market capitalization is $511 billion and Chevron’s is $291 billion, ConocoPhillips lands at $134 billion.

The deal’s documents bake antitrust risk into the agreement, nevertheless. According to DealPulse’s M&A database, which harnesses both AI and attorneys to digest the granular deal points of publicly announced transactions, ConocoPhillips’s 8-K filing includes standard antitrust language:

The completion of the Merger is subject to satisfaction or waiver of certain customary mutual closing conditions, including (1) the receipt of the required approvals from Marathon stockholders, (2) the expiration or termination of the waiting period under the Hart-Scott-Rodino Antitrust Improvements Act of 1976, as amended (the HSR Act), (3) certain other specified regulatory approvals having been obtained, (4) the absence of any governmental order or law that makes consummation of the Merger illegal or otherwise prohibited …

Further, the merger agreement bakes possible antitrust action throughout, including the termination terms and covenants and agreements sections. For example, this deal’s agreement details:

Each Party shall: (i) promptly notify the other Parties of, and if in writing, furnish the others with copies of (or, in the case of oral communications, advise the others of the contents of) any communication to such Person from an Antitrust Authority or other Governmental Entity and permit the others to review and discuss in advance (and to consider in good faith any comments made by the others in relation to) any proposed written communication to an Antitrust Authority or other Governmental Entity

Such language has become standard in most U.S. deals, with attorneys customizing according to specific clients’ circumstances.

ConocoPhillips is advised by Wachtell, Lipton, Rosen & Katz and Marathon is advised by Kirkland & Ellis LLP.