On the heels of Cadent’s announcement of its intentions to acquire machine learning pioneer AdTheorent in a $324 million all cash deal, a third party has arrived with a higher bid. Although the merger with Cadent was unanimously approved by AdTheorent’s board of directors for $3.21 per share, the merger agreement included a go shop provision that permitted AdTheorent to seek alternative suitors for 33 days — and an unnamed suitor indeed has offered $3.35 per share.

Just last month, Eric Tencer, AdTheorent’s Chairman of the Board, lauded the deal, stating “this transaction delivers immediate, certain and significant value to the Company’s shareholders reflecting the tremendous commitment and work of our employees and stakeholders.”

Nevertheless, AdTheorent negotiated a period where would actively seek a better offer to purchase the company – and this “go shop” provision may very well derail its announced merger with Cadent.

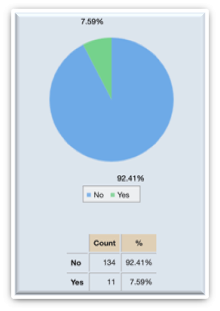

Go shop provisions first appeared in 2004 with Welsh, Carson, Anderson & Stowe’s acquisition of US Oncology and remain relatively rare. According to DealPulse’s M&A database, which harnesses both AI and attorneys to digest the granular deal points of each publicly-announced transaction over $25 million, just 7.6% of mergers in the business services industry over the past 5 years included a go shop provision. This is slightly higher than the 6.8% rate for deals across industries over the past 15 years.

Frequency of Go Shop Provision in Business Services Industry 2019-2024

Although go shop provisions most often appear when a private company is being purchased by private equity shop, they are becoming more common when a public company is going private, just as the public AdTheorent would be doing if purchased by private company Cadent. Some criticize these provisions as “a fig leaf to provide cover for management to seal the deal with its preferred bidder, while insulating the board against claims that it failed to satisfy its obligation to maximize value for the shareholders in the sale of the company,” as one published in the Harvard Law Review describes it. It cites a previous study finding that go shop provisions yield a higher bidder 13% of the time.

Where will AdTheorent and Cadent go from here? Under the terms of their merger agreement, AdTheorent will now review the proposal from the third-party bidder and determine whether the higher price indeed constitutes a superior offer. If so, AdTheorent will inform Cadent of its intention to terminate the merger, though Cadent has match rights than provide it with an opportunity to amend its offer to match the superior one from the other suitor.

AdTheorent is advised by law firm McDermott Will & Emery, and financial adviser

Canaccord Genuity LLC. Cadent is advised by Baker Botts LLP, and financial advisor Moelis & Company