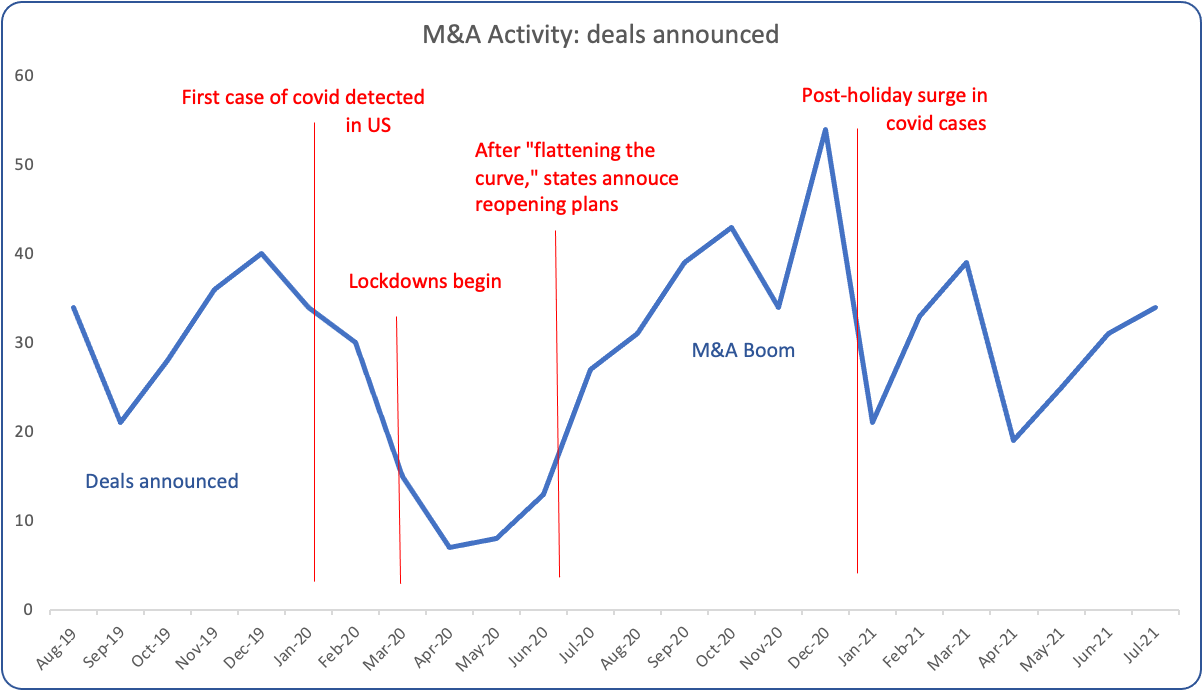

The United States mergers & acquisitions (M&A) market has faced a turbulent period, fluctuating wildly during the COVID-19 pandemic. Matterhorn’s M&A database tracks publicly-announced deals over $25 million in value, harnessing a combination of natural language processing, machine learning, and attorneys to digest the granular deal points of each transaction to allow for comparisons across industries, specific deal terms, and both legal and financial advisors.

As the country “flattened the curve” during the late spring of 2020, states began announcing plans to ease their lockdowns. Fueled but the flood of cheap financing available after the Federal Reserve slashed rates, M&A activity boomed. Deal volume during September to December 2020 far exceeded activity during comparable pre-pandemic periods, representing a 35.2% increase over 2019 levels.

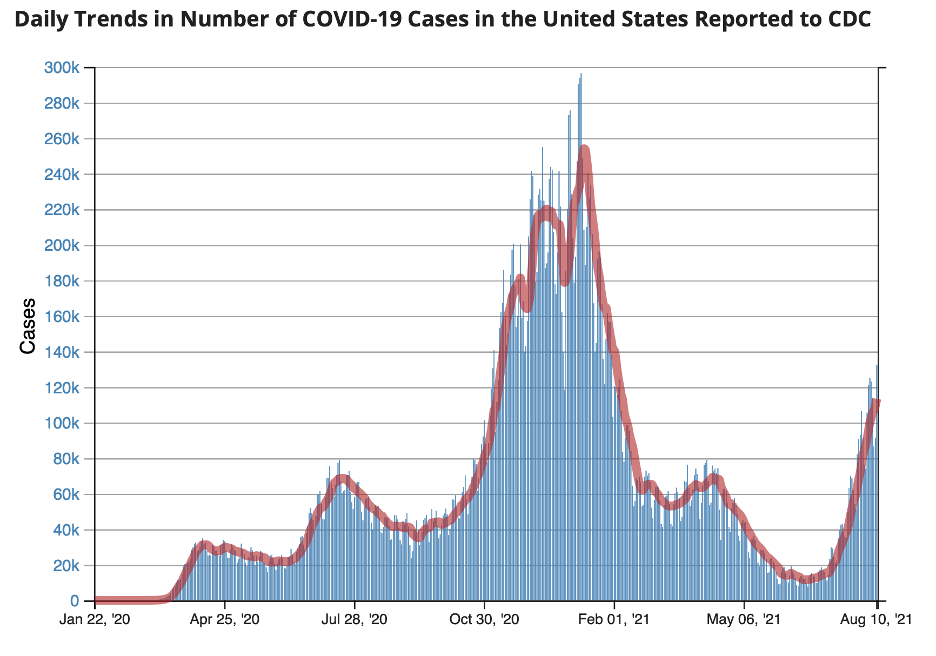

Although M&A volume traditionally falls in January each year, January 2021 saw a precipitous decline of 61%. This drop coincided with the United States’ peak in COVID-19 cases following the holiday.

As cases declined from February until March 2021, M&A activity rebounded partially before faltering again in April. Deal activity then enjoyed a gradual increase during the end of spring and start to the summer but now as cases spike again with the Delta variant, history indicates that M&A activity may falter yet again.

Securities Litigation: A Similar Story

Docket Alarm analysis over the same period of time (August 2019 to August 2021) reveals that securities litigation follows a similar, but not identical pattern to that of high-dollar transactions generally.

Spikes in PACER cases tagged as securities litigation can be observed in September 2020 as M&A activity resumed. However, unlike the trend for transactions, securities litigation generally picked up in the early months of the pandemic, perhaps driven in part by businesses like Zoom, which enjoyed unprecedented usage of its services which was soon followed by increased scrutiny of its security and privacy practices.

As the pandemic ebbed in the second quarter of 2021, securities litigation remained quite active; time will tell if this trend continues as economies react to the spread of the Delta variant.

Political Winds

The pandemic is not the only force driving the M&A market. Both expectations regarding rising tax rates and a more aggressive antitrust policy under the new administration affect deal activity.

Case in point: Aon Plc and Willis Towers Watson Plc terminated their multi-billion merger, which had sought to create the largest insurance broker in the world. This termination comes with a whooping price tag: according to the Willis Towers Watson 8-K filing from March 2020, “In the event the Business Combination Agreement is terminated in connection with certain circumstances related to the failure to receive the antitrust and competition clearances that are conditions to closing, Aon would be obligated to pay a fee of $1 billion.”

The deal fell apart mere weeks after the U.S. Department of Justice sued to block the deal due to antitrust concerns. This was in stark contrast to the more lenient stance adopted by European regulators, who had approved previously approved the deal between the two London-based companies after they agreed to divest certain assets. In what has been hailed as a win for the Biden Administration as it pushes for a more muscular antitrust policy, the two companies ultimately agreed to abandon their efforts to fight the DOJ’s suit.

This turn of events may further cool the M&A market as larger firms potentially face similar government scrutiny.

Willis Towers Watson was advised by law firms Weil, Gotshal & Manges LLP and Skadden, Arps, Slate, Meagher & Flom LLP, and financial advisor Goldman Sachs & Co. LLC. Aon was advised by law firms Latham & Watkins LLP and Freshfields Bruckhaus Deringer LLP, and financial advisor Credit Suisse Securities LLC.

Logan Beirne is a lawyer, entrepreneur, and academic. He serves as CEO of Matterhorn Transactions, Inc., an AI-powered tech company that provides M&A analytics to thousands of law firms across the US, UK, and Canada. In addition to its public deal systems, Matterhorn also customizes and hosts databases of private deal-related documents for law firms. Using proprietary software and analytic expertise, Matterhorn’s databases provide unprecedented insight into proprietary deal-document databases, and significantly enhance precedent management and analysis.

Logan has served on the board of directors of 5 organizations and the board of governors of a municipality. He also teaches Financial Markets, Corporate Law, and Business Ethics at Yale Law School. His bestselling book, Blood of Tyrants: George Washington, the Forging of the Presidency, won the 2014 Colby Award and the Lincoln Medal. Beirne and his writings have been featured by The New York Times, The Wall Street Journal, USA Today, The Washington Times, Reuters, National Review, and other media outlets.

Previously, Logan was an attorney at Sullivan & Cromwell LLP and worked in private equity at GE Capital. He received his BS from Fairfield University, was a Fulbright Scholar at Queen’s University, and received his JD from Yale Law School.