Even as the omicron variant of COVID-19 threatens the world economy, U.S. M&A activity continues to boom. Just as the rest of the world economy has worked to adapt to the pandemic, the U.S. M&A market has evolved in the face of the tumult: attorneys have quickly adapted agreements’ language to reflect the ever changing uncertainties of the new era. Matterhorn’s M&A database tracks the indelible marks that COVID-19 has left on M&A transactions by harnessing both AI and attorneys to digest the granular deal points of each publicly announced deal over $25 million in value.

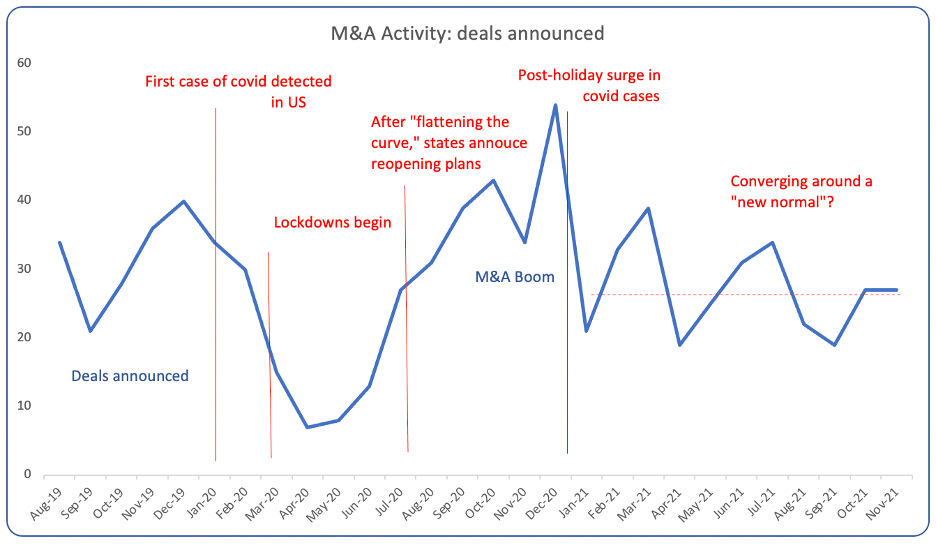

Initially, the pandemic’s onslaught led to vast turbulence in deal activity. Deal terminations surged during the first half of 2020, before declining over the summer as cash flooded the market and an M&A boom emerged during the second half of the year. The following chart depicts the highs and lows of pandemic deal activity. While 2021 has faced relatively less tumult, the emergence of the omicron variant will test the market’s resiliency.

Source: Matterhorn Transactions

And the volume of deals announced only tells part of the story – the M&A market predicted to hit a record $6 trillion in deal activity this year. Activity has flourished during the pandemic by updating deal language to reflect the new risks. The mergers, asset purchases, and stock purchase agreements tracked by Matterhorn reflect a lasting mark on term language. In addition to the rise of practical changes like remote closings, the COVID-19 related material adverse effects (MAE) clauses and interim operations covenants are becoming standard.

For example, Commercial Metals Company’s $550 million private target merger with TAC Acquisition Corp. last week addresses COVID-19 13 times within its deal documents. It includes the cautionary statement in its press release and 8-K“Important factors that could cause actual results to differ materially from our expectation: … impacts from COVID-19 on the economy, demand for our products, global supply chain and on our operations, including the responses of governmental authorities to contain COVID-19 and the impact from the distribution of various COVID-19 vaccines.” As is becoming market standard, the deal’s merger agreement explicitly includes COVID-19 in both its MAE act of God and changes in legal or regulatory conditions clauses, as well as a blanket “the effect of any COVID-19 Measure.”

With an eye on omicron, Compagnie de Saint-Gobain $2.3 billion acquisition last week of GCP Applied Technologies included the MAE language: “changes due to the outbreak or worsening of an epidemic, pandemic or other health crisis (including COVID-19, or any COVID-19 Measures or changes in such COVID-19 Measures after the date of this Agreement).” And if the spikes in cases abroad are an indication, the latest variant may very well come to fit that clause.

These terms will continue to evolve. As attorneys draft coming deals, they will need to provide flexibility in their language: e.g. deals have very recently begun to address vaccination, but “fully vaccinated” may soon change to include booster shots, which will affect deals already using the term. We will surely see further innovation in deals’ clauses as M&A booms into 2022.