Even as some analysts warn of “a death spiral for SPACs,” United Gear & Assembly, Inc., a subsidiary of United Stars Holdings, Inc., announced plans to go public via a SPAC acquisition by Aesther Healthcare Acquisition Corp. Upon closing of the $350 million merger, Aesther will change its name to EVGT LTD and its common stock is expected to be listed on Nasdaq, under the symbol EVGT, and its warrants listed under EVGTW.

But like a shark driven from its traditional feeding ground by lack of prey, this merger is afield from the SPAC’s original focus. United Gear manufactures high precision gears for electric vehicles and other industries. Its client base includes EV-maker Lucid as well as traditional automatic companies Volvo, HUSCO, Dana and GM. Beyond cars, United Gear provides for the construction, mining, and agricultural markets.

As its name indicates, “Aesther Healthcare Acquisition Corp.” was intended to focus on the healthcare industry rather than gears. But while some SPACs include an industry mandate, they need not. In its July 2021 Form S-1 filing, states “While we may pursue an initial business combination target in any business or industry, we intend to focus our search on industries that complement our management team’s background and to capitalize on the ability of our management team to identify and acquire a business focusing in the pharmaceutical and medical devices sectors, where our management team has extensive experience.” And this transaction represents an example of a SPAC seeking to invest in areas outside their intended focus rather than wind down.

SPACs do not last forever. They are required to close a deal over a defined period or otherwise return the funds to their investors. As Bloomberg summarizes the Aesther/United transaction, “A blank-check company that set its sights on buying a business in health care is taking on an industrial firm instead as empty-handed SPACs try to beat deadlines that would force them to shut down.” As of May 2022, there were an estimated backlog of 600 SPACs that needed to ink a deal or otherwise wind down.

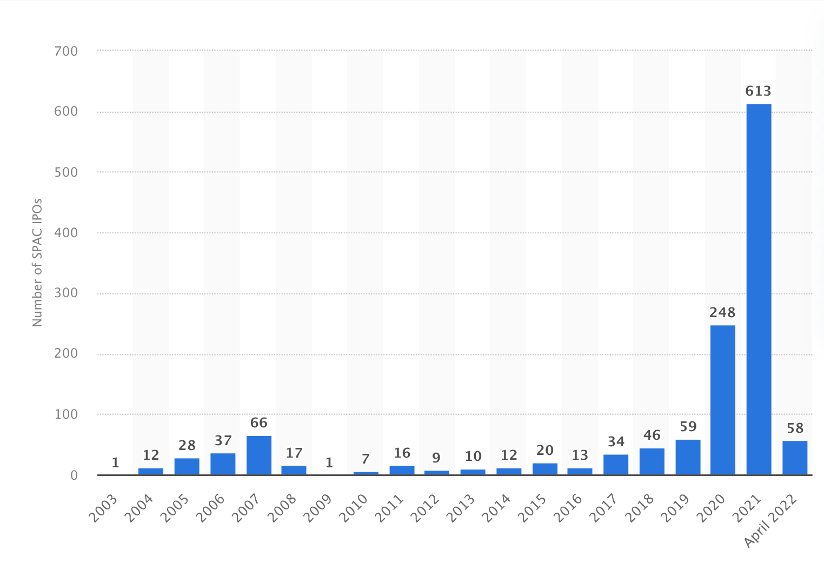

SPAC IPOs in the United States 2003 – April 2022

Source: https://www.statista.com/statistics/1178249/spac-ipo-usa/

As the stock market has plunged, SPACs have found it increasing difficult to find targets. And even deals previously signed have unwound. High profile deals, such as the plan for Forbes to go public via SPAC, have fallen apart as the IPO market suffers. This has promoted headlines such as, “SPAC Era Comes to a Whimpering End.”

According to Matterhorn’s comprehensive M&A database, which harnesses AI to track current and historical deals, Aesther was advised by law firm Ellenoff Grossman & Schole LLP. United Gear was advised by law firm Barack Ferrazzano Kirschbaum & Nagelberg LLP and financial adviser Colonnade Securities LLC.